{kind=link}

[ad_1]

Managing roughly $19 billion in shopper property throughout hundreds of portfolios is a frightening process. However Allworth Monetary Chief Funding Officer Andy Stout has a disciplined course of to allocating shopper property. Actually, the agency has a 20-page guide that describes its whole funding course of.

Right here, Stout provides a peak contained in the Folsom, Calif.-based RIA’s core/satellite tv for pc mannequin portfolio, the agency’s fund choice course of and its use of direct indexing and options.

This interview has been edited for type, size and readability.

WealthManagement.com: What’s in your mannequin portfolio?

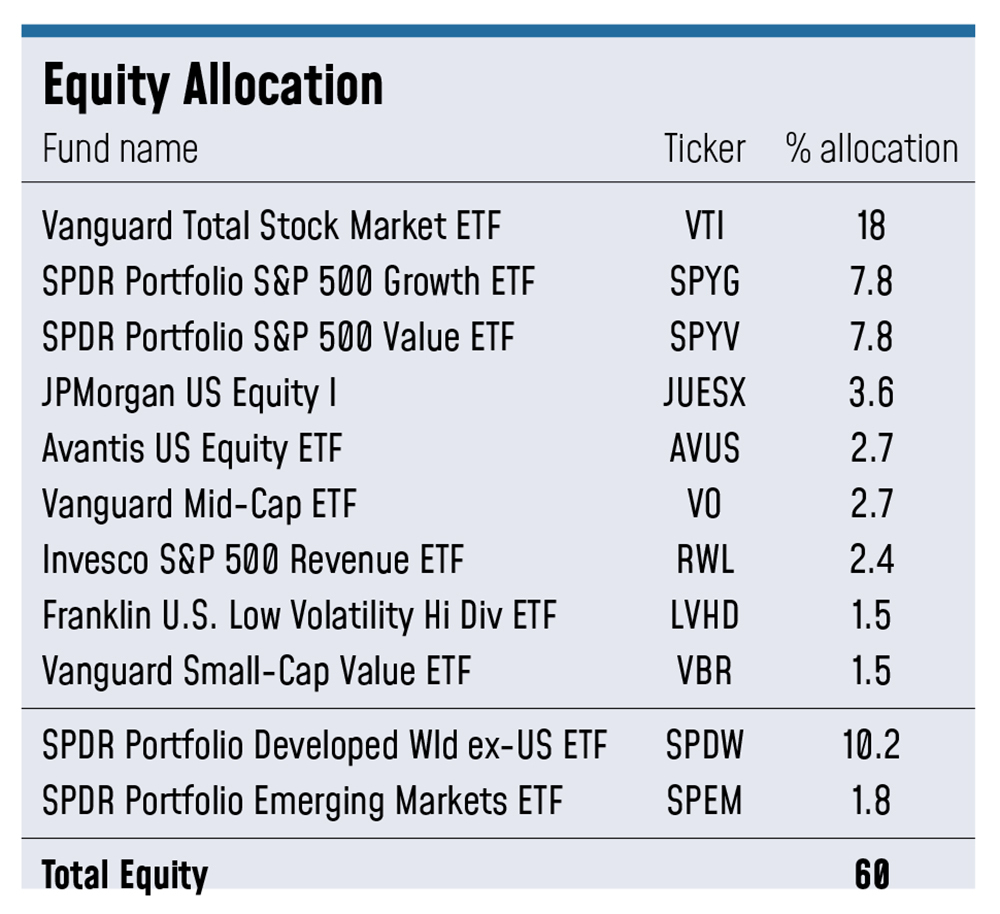

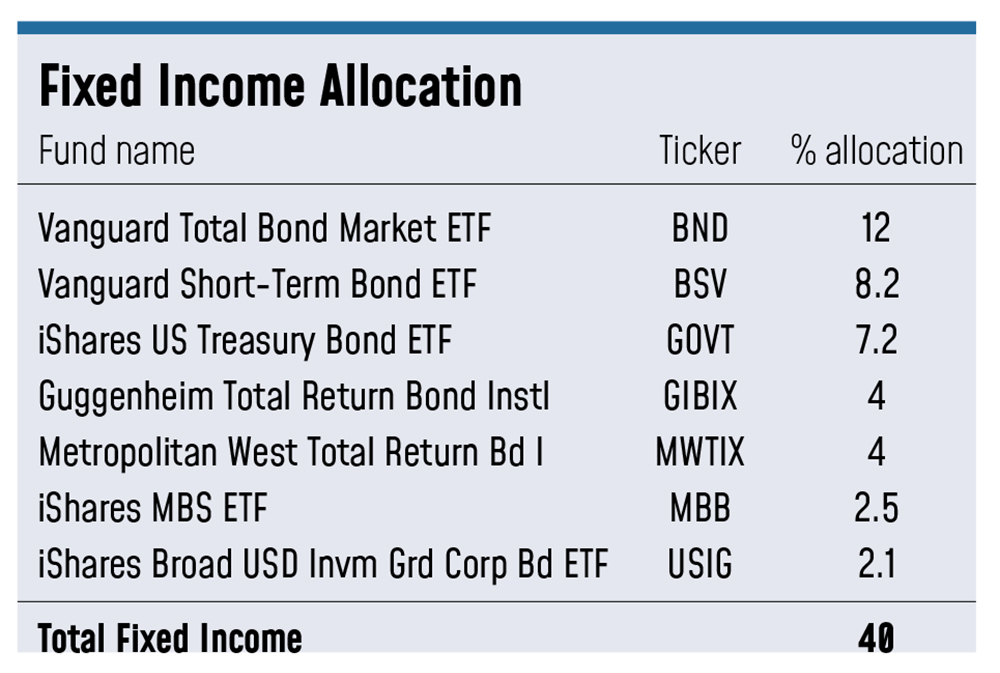

Andy Stout: I’ll use one among our fashions, our core/satellite tv for pc 60/40 portfolio as a proxy. We use a mixture of energetic and passive funds. So throughout the 60 a part of the 60/40, we’ve a cut up 48% U.S., 12% worldwide shares. The mounted earnings portion is a mixture of short-term bond funds, funding grade and complete return funds. We’ve just a few energetic managers in there, making an attempt to navigate the market.

WM: What asset managers do you utilize, if any?

AS: We deliberately unfold out our allocations amongst many alternative managers, as a result of we clearly do not need to turn out to be the market. And meaning we’ve SPDR, Vanguard, BlackRock, JP Morgan. These usually signify what we’ll name our core a part of the core satellite tv for pc. Extra on the satellite tv for pc aspect, you would possibly see just a little bit extra of tilts might be one phrase for it, or simply an energetic allocation, if you’ll. For instance, we’ve a barely extra tilt to worth than development.

Now that is extra a perform of not essentially us liking worth over development, however the funds that we’ve chosen on the satellite-side fall extra on the worth type field, if you’ll. So, for instance, we’ve a revenue-weighted ETF, and a low-volatility, high-dividend ETF in our satellite tv for pc portion. That is by Invesco—the Invesco income ETF is RWL. And the low-volatility ETF is from Franklin. That is extra of wanting on the enterprise cycle and seeing the place dangers are, and the place we need to mitigate these dangers.

On the mounted earnings aspect, we use Vanguard, iShares, SPDR. We even have some energetic funds in there, corresponding to Guggenheim’s Complete Return Bond fund, which is GIBIX, and Metropolitan West’s Complete Return Fund, MWTIX.

We like these funds as a result of they’ve traditionally finished a great job of navigating a full enterprise cycle and full funding cycle. They will not all the time be hitting house runs each quarter, however we’re wanting extra for the singles and doubles and consistency. Once we take into consideration serving our purchasers, you need not hit a house run on a regular basis, however in case you strike out quite a bit, you are going to put the purchasers in a troublesome scenario, and we do not need to jeopardize their monetary objectives. So, it is actually vital to be sure that we concentrate on consistency and decrease volatility whereas nonetheless having the ability to take part within the upside.

WM: The place are the dangers proper now?

AS: Recession danger is elevated, and I do not assume anyone would actually query that. I do know there is definitely a distinction of opinion on whether or not or not there will be a comfortable touchdown or not. I am not making an attempt to make a recession name right here in any respect. However what we’re making an attempt to do is place the portfolios in a fashion the place we consider a number of chances of varied attainable future states of the economic system. That leads us to see that the financial dangers are extra elevated. That is the place the draw back dangers are. In consequence, we need to improve publicity to safety varieties that might higher climate within the financial storm that manifests.

WM: What components go into your fund choice?

WM: What components go into your fund choice?

AS: Each month we’ve our personal proprietary scorecard the place we rating greater than 20,000, mainly the entire investable universe of mutual funds and ETFs. This proprietary scorecard appears to be like at greater than 100 completely different variables and permits us to primarily take into consideration the universe in a a lot smaller pattern, primarily based on these indicators. And that primarily bubbles up funds that we expect are price a more in-depth look. Then we are going to speak with the varied portfolio managers which are on that listing to find out if we imagine they’ve some type of repeatable course of that might result in alpha.

WM: What are some examples of these 100 variables you’re taking a look at?

AS: It’s every thing from expense ratio to Sortino ratio, Treynor ratio, Sharpe ratios, over varied time intervals. It tracks returns relative to benchmarks so far as alpha goes, then additionally volatility. We’re taking a look at a myriad of return measures, danger measures, and risk-return measures over varied time intervals.

Then, we’ll separate them by completely different asset classes or asset lessons as a result of some sectors would possibly simply all the time have a decrease rating than different sectors. So, we are going to apply a percentile rank inside every sector or asset class to see the highest scoring funds, after which primarily we decide how a lot weight we need to put into every asset class as effectively.

WM: Have you ever made any huge funding allocation adjustments within the final six months to a yr? If that’s the case, what adjustments?

AS: A few issues that we’ve deliberately finished over the course of 2023 is to enhance the general credit score profile, which means it is larger high quality fixed-income in comparison with the place we have been earlier within the yr. However in case you have a look at credit score spreads, they’re very tight proper now. Additionally, we’ve truly elevated our length over the previous few months deliberately. We had a a lot decrease length to begin 2023.

Now we’re as much as the purpose the place our length is at about 5.6 years, so it is a lot larger than what it has been anytime up to now few years. It was in all probability round 4.2 years a yr or so in the past. Whenever you have a look at the rate of interest setting, it does seem that the Federal Reserve is—if they don’t seem to be finished climbing charges—they’re seemingly very near finished climbing charges. And most definitely, not less than primarily based on market chances, they’d lower charges in 2024. 4 quarter level fee cuts are at the moment priced in. We need to make the most of that. So, we nonetheless get the sturdy yield, which you may get on longer-term and shorter-term bonds, however we’d get extra worth appreciation by being just a little additional out within the yield curve.

On the fairness aspect, we added the revenue-weighted fund and the low-volatility fund throughout the final six months. It is keying off of our view that if you’re wanting on the varied financial states that might happen, there’s some barely extra dangers to the draw back than there are to the upside. We do not imagine it is ever prudent to go multi function manner or one other, and we cannot market time both. That’s usually a idiot’s errand.

WM: What differentiates your portfolio?

WM: What differentiates your portfolio?

AS: It is actually essential to have diversification, publicity to broad asset lessons and have a disciplined course of once you’re constructing these portfolios. All too usually I’d see individuals making emotional choices, even skilled traders. Our course of is each qualitative and quantitative by way of figuring out investments, but additionally figuring out asset lessons that is likely to be extra engaging than others. And by sticking to our disciplined course of, that permits us to not fall sufferer to emotional decision-making. We’ve a 20-page guide that basically describes our entire funding course of behind the scenes.

Additionally, a agency like ours, we will have a whole lot of completely different funding choices. We’ve different mixes of energetic and passive, some the place we embrace liquid options. We’ve an all passive, we’ve income-oriented methods, factor-oriented mannequin suites. Once I take into consideration what makes us completely different, it’s that we perceive there is not a one-size-fits-all mannequin portfolio. We need to be sure that we’ve funding choices which are engaging to purchasers and advisors throughout the board.

WM: Do you allocate to non-public investments and options? If that’s the case, what segments do you want?

AS: We do have different property that the advisors can select in the event that they imagine it’s within the shopper’s finest curiosity. That features personal fairness, hedge funds, personal debt, personal actual property. There is a market-neutral fund. We’ve a Certified Alternative Zone fund as effectively.

We’ve an inner restrict the place we would not put greater than 25% of the shopper’s property in options or illiquid options. It relies on what the shopper wants. Some purchasers do not want tax deferral, like you may get with a certified alternative zone. We’ve a pair funds that do a fairly good job at producing earnings. One other one is concentrated on enhancing returns.

WM: How a lot do you maintain in money? Why do you maintain money?

AS: We’re not chubby money from a firm-wide perspective. Usually, we maintain 1% in money. We do this outdoors of the mannequin, day finish. If they’ve any ongoing distributions, we’ll often maintain about 4 months of money available for that as effectively.

Our advisors do have the flexibility to put money into money outdoors of no matter we would pull usually. So, we’ve many alternative money choices for advisors to select from. The high-yield cash market funds, no matter CDs can be found—often we’ll undergo the custodian for that.

If the purchasers have these short-term money wants, we’re more than pleased to fulfill that. As a result of you do not have to simply maintain your cash in a financial institution if you wish to earn some curiosity. You would in all probability get just a little bit extra outdoors of a financial institution anyway, in comparison with most locations. You possibly can usually get larger charges shopping for a treasury invoice.

WM: Do you utilize direct indexing? If that’s the case, why? Do you utilize an asset supervisor or tech supplier for that?

AS: Sure, we use Aperio for our direct indexing wants.

There are such a lot of statistics on the market that recommend it is onerous for energetic managers to beat their index. Does that imply there is no such thing as a such factor as alpha? No, there’s tax alpha. It simply takes some work. This takes a whole lot of simply getting down into the weeds and figuring issues out. The rationale I like Aperio, is as a result of they’ve proven outcomes the place they’ve added a whole lot of tax alpha on a fairly common foundation for his or her traders. And one other factor I like about direct indexing is, if a shopper occurs to be charitably-inclined, then we will donate essentially the most appreciated inventory and decrease the shopper’s general tax foundation.

WM: Are you incorporating ESG into the portfolio? If that’s the case, how?

AS: We do have an ESG mannequin suite. We don’t incorporate ESG into any of our different fashions. So if the shopper needs ESG, they usually explicitly ask for it, that is after we would supply them our ESG methods. However in all the opposite methods, ESG is just not a consideration in any respect.

The ESG mannequin suite was designed by screening for funds that had an specific funding goal to be targeted on ESG, or SRI, or no matter nomenclature you need to use. It’s explicitly said of their fund’s goal that is what they’re doing. Then what we have finished, is have a look at the rankings out of Morningstar, or danger management metrics for environmental, social, and governance. Then, we optimize it to reduce these for poor governance management. Then, throughout that optimization course of, we’re making use of constraints in order that the general inventory, U.S. shares, worldwide shares, are just like our different methods. And company bonds to authorities bonds, these are additionally just like our different methods. So whereas we do have many alternative funding methods and mannequin suites out there, all of them sing from the identical songbook, if you’ll.

[ad_2]