{kind=link}

[ad_1]

I used to be poking across the Bogleheads discussion board after I found this thread about an interval fund.

I’ve heard of every kind of funds, however that is the primary time I’ve heard about interval funds. Concerning funds, I’m just about an index mutual fund or index exchange-traded fund (ETF). They’re all at Vanguard, although I feel Constancy, Charles Schwab, and all the opposite low-cost suppliers are nice, too.

Interval funds are a totally totally different animal, and, on this case, the unique poster invested in a Variant Various Earnings Fund (NICHX):

Thanks upfront in your time. Two years in the past I used to be coping with some nervousness in my life. My spouse and I made the choice to enlist an advisor to handle a portion of our holdings. That turned out to not be the precise factor to do and he didn’t serve us effectively. We have now terminated his contract and now I’m working to reallocate our accounts into extra acceptable funds.

He invested a not-insignificant quantity of funds right into a Variant Various Earnings Fund (NICHX). I assume it’s thought of an “interval fund.” That I can solely exit quarterly. The worth-per-share has been flat, but it surely pays an honest quarterly dividend that’s robotically reinvested. An preliminary funding of $103k in late 2022 has paid over $15k in dividends over six quarters (545 new shares).

This after all triggers the very nervousness I battle with. My intention was to get to a 70/30 AA. I assume my choices are:

1) Get out of the fund as quickly as the subsequent quarterly-sell interval opens.

2) Maintain all or some and attribute it both to the fairness facet or the bond/money facet of my AA.

3) Maintain all or a few of it, however go away it outdoors of my AA (which means faux it’s not there).Your knowledge is welcome.

Desk of Contents

What’s an Interval Fund?

An interval fund is a mutual fund that may be a closed-end fund the place you may solely promote your shares throughout a repurchase interval. This era varies from fund to fund however many are on a quarterly interval and the fund will state what number of of their excellent shares they are going to repurchase (redeem), normally acknowledged as a share.

In case you learn “closed-end fund” after which “redemption durations” and already knew what a closed-end fund was, this might be complicated. Sometimes, closed-end funds problem shares at an IPO after which by no means purchase them again. The shares can commerce on the open market, however new cash doesn’t return into the fund.

With an interval fund, they’re in between open-end and closed-end funds as a result of they’ll provide new shares however solely redeem them at numerous intervals (quarterly, semi-annually, and so on.) and just for a set share of property.

I wager you may see how issues get tough as a result of this fund is comparatively illiquid. If an interval fund says they’ll repurchase 10% and greater than 10% of the shares need to be repurchased, everybody will get pro-rated down.

This construction advantages the interval fund as a result of a number of redemptions may cause issues for the fund, because it has to provide you with the cash to offer again to shareholders. With a set cadence for coping with redemptions, the supervisor can plan for them (each in timing and dimension).

The scheduled redemptions enable managers to spend money on extra complicated securities and contracts, which can themselves be extra illiquid.

NICHX: Peek at an Interval Fund

The Bogleheads submit talked about NICHX, so I believed I’d look nearer at this.

NICHX is attention-grabbing – it invests in unconventional income-generating property like litigation finance, royalties, and so on. It’s a fixed-income fund, so don’t examine it to an S&P 500 index, and it invests in different money circulation property that I’ve checked out beforehand.

It’s an interval fund that doesn’t commerce on the open market, so the one option to promote your shares is thru NICHX. Not like many interval funds, although, there doesn’t seem like a gross sales cost.

You’ll be able to see that NICHX compares itself with many fixed-income property, such because the Bloomberg U.S. Combination Bond Index and Bloomberg U.S. Excessive Yield Bond Index, which appears affordable. They beat the utterly principal-safe T-bills and examine favorably with high-yield company bonds and the like.

With interval funds, it’s essential to grasp the strategy and asset lessons that they spend money on, in addition to the charges. These funds do much more than monitoring an index, in order that they usually cost far more.

For NICHX, we see that they’ve a web expense ratio of 1.67% (which incorporates the Administration payment of 0.95%). Additionally, NICHX solely permits a quarterly redemption of 5% of the fund’s web asset worth.

Is that this costly? It seems costly in comparison with an S&P500 Index fund that costs you solely 0.04%, however that’s not a good apples-to-apples comparability as a result of they’re invested in numerous issues with totally different threat profiles.

You need to examine it with one thing that invests in different investments.

Yieldstreet Various Earnings Fund

Yieldstreet provides a Yieldstreet Various Earnings Fund that benchmarks towards the Bloomberg U.S. Combination Bond Index and Bloomberg U.S. Excessive Yield Bond Index. It invests in income-producing different property like business actual property, plane, authorized finance, provide chain finance, artwork finance, and so on.

In addition they restrict redemptions to twenty% of shares excellent within the prior calendar 12 months or not more than 5% in every quarter, on a quarterly foundation—the identical as NICHX.

As for charges? 1.50%. It’s barely cheaper than NICHX however inside the similar ballpark. (no gross sales load both)

The half that’s barely complicated about this fund is that they record this as their charges:

If that’s laborious to see:

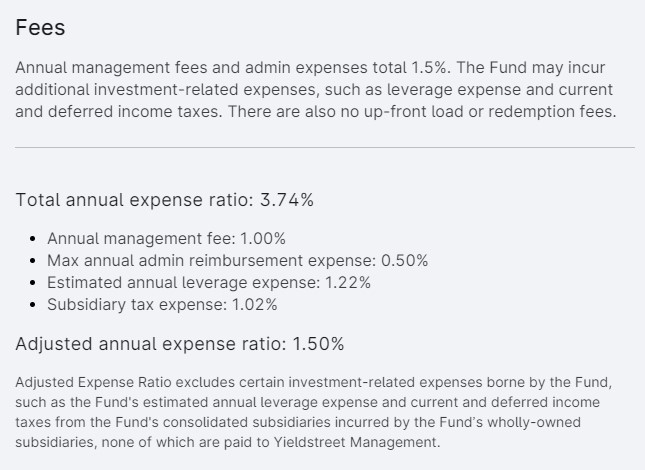

Charges

Annual administration charges and admin bills whole 1.5%. The Fund could incur extra investment-related bills, equivalent to leverage expense and present and deferred earnings taxes. There are additionally no up-front load or redemption charges.

Whole annual expense ratio: 3.74%

- Annual administration payment: 1.00%

- Max annual admin reimbursement expense: 0.50%

- Estimated annual leverage expense: 1.22%

- Subsidiary tax expense: 1.02%

Adjusted annual expense ratio: 1.50%

Adjusted Expense Ratio excludes sure investment-related bills borne by the Fund, such because the Fund’s estimated annual leverage expense and present and deferred earnings taxes from the Fund’s consolidated subsidiaries incurred by the Fund’s wholly-owned subsidiaries, none of that are paid to Yieldstreet Administration.

The three.74% consists of “estimated annual lever expense” and “subsidiary tax expense,” that are gadgets we don’t see in NICHX. I’m undecided why they embrace them as they don’t seem to be paid to Yieldstreet. Maybe they’re included within the returns of different funds (different funds could have related bills, although I don’t typically see them itemized like this).

The 1.50% itself, although, is on par with NICHX.

In doing extra analysis on interval funds, you’ll discover that they’ve greater charges, although, so the 1.69% at NICHX and the 1.50% from Yieldstreet are typical. You gained’t see payment buildings like index funds, and that is smart; these funds execute complicated transactions and don’t simply observe an index.

Do You Want Interval Funds?

Right here’s the large query – do you must spend money on interval funds?

I’d argue most individuals don’t.

In case you have a look at the unique poster from Bogleheads, his advisor put not less than one million bucks (that’s the minimal for NICHX) into this fund, and he wasn’t even positive why. That’s a foul signal. In case you don’t perceive, you must hold asking questions till you do. They be just right for you, and if they’ll’t clarify it, they aren’t ok.

As for interval funds on the whole, are the returns that a lot better to justify the illiquidity? You’ll be able to solely get 5% out each quarter, so at a minimal, you’re speaking 5 years to exit the holding absolutely… and that’s for those who don’t get pro-rated.

The 1.50%+ payment must also be an enormous concern. The payment could also be justified, but it surely doesn’t imply you should purchase the product. With investing, we’ve got extra management over the price than the returns, so paying a better payment means our funding has a a lot greater hurdle to beat.

For many, you might be higher off with a easy three-fund portfolio or one thing equally easy. There could also be some circumstances the place you’d need one (and maybe one which invests in one thing else). However for many, it’s a go. (heck, earlier than you ever get to the upper price, the illiquidity is sufficient to make me balk)

As for this asset class, “different investments” are enjoyable to examine and examine, however they’re hardly required in any portfolio. I personal some farmland by AcreTrader and artwork by way of Masterworks, however that’s small quantities for enjoyable somewhat than as a result of I feel they’re a mandatory a part of my portfolio.

[ad_2]