")

{kind=link}

[ad_1]

Up to date on January 28, 2024 with up to date screenshots from TurboTax Deluxe downloaded software program. Should you use different tax software program, see:

Should you did a Backdoor Roth, which includes making a non-deductible contribution to a Conventional IRA after which changing from the Conventional IRA to a Roth IRA, you want to report each the contribution and the conversion within the tax software program. For extra info on Backdoor Roth, see Backdoor Roth: A Full How-To.

What To Report

You report on the tax return your contribution to a Conventional IRA *for* that 12 months, and also you additionally report your conversion to Roth *throughout* that 12 months.

For instance, if you find yourself doing all of your tax return for 12 months X, you report the contribution you made *for* 12 months X, whether or not you truly did it throughout 12 months X or the next 12 months between January 1 and April 15. You additionally report your conversion to Roth *throughout* 12 months X, whether or not the contribution was made for 12 months X, the 12 months earlier than, or any earlier years.

Due to this fact a contribution made throughout the next 12 months for 12 months X goes on the tax return for 12 months X. A conversion finished throughout 12 months Y after you made a contribution for 12 months X goes on the tax return for 12 months Y.

You do your self a giant favor and keep away from quite a lot of confusion by doing all of your contribution for the present 12 months and ending your conversion in the identical 12 months. I known as this a “deliberate” Backdoor Roth — you’re doing it intentionally. Don’t wait till the next 12 months to contribute for the earlier 12 months. Contribute for 12 months X in 12 months X and convert it throughout 12 months X. Contribute for 12 months Y in 12 months Y and convert it throughout 12 months Y. This fashion every thing is clear and neat.

If you’re already off by one 12 months, catch up. Contribute for each the earlier 12 months and the present 12 months, then convert the sum throughout the identical 12 months. See Make Backdoor Roth Simple On Your Tax Return.

Use TurboTax Obtain

The screenshots under are from TurboTax Deluxe downloaded software program. The downloaded software program is method higher than on-line software program. Should you haven’t paid in your TurboTax On-line submitting but, you should purchase TurboTax obtain from Amazon, Costco, Walmart, and plenty of different locations and change from TurboTax On-line to TurboTax obtain (see directions for make the change from TurboTax).

Right here’s the deliberate Backdoor Roth situation we are going to use for example:

You contributed $6,500 to a standard IRA in 2023 for 2023. Your revenue is simply too excessive to say a deduction for the contribution. By the point you transformed it to Roth IRA, additionally in 2023, the worth grew to $6,700. You don’t have any different conventional, SEP, or SIMPLE IRA after you transformed your conventional IRA to Roth. You didn’t roll over any pre-tax cash from a retirement plan to a standard IRA after you accomplished the conversion.

In case your situation is totally different, you’ll have to make some changes to the screens proven right here.

Earlier than we begin, suppose that is what TurboTax reveals:

We are going to evaluate the outcomes after we enter the Backdoor Roth.

Convert Conventional IRA to Roth

The tax software program works on revenue gadgets first. Although the conversion occurred after the contribution, we enter the conversion first.

Whenever you convert from a Conventional IRA to a Roth IRA, you’ll obtain a 1099-R type. Full this part provided that you transformed *throughout* the 12 months for which you’re doing the tax return. Should you solely transformed throughout the next 12 months, you gained’t have a 1099-R till subsequent January. Skip all the way in which to the subsequent part: Non-deductible contribution to Conventional IRA.

In our instance, we assume by the point you transformed, the cash within the Conventional IRA had grown from $6,500 to $6,700.

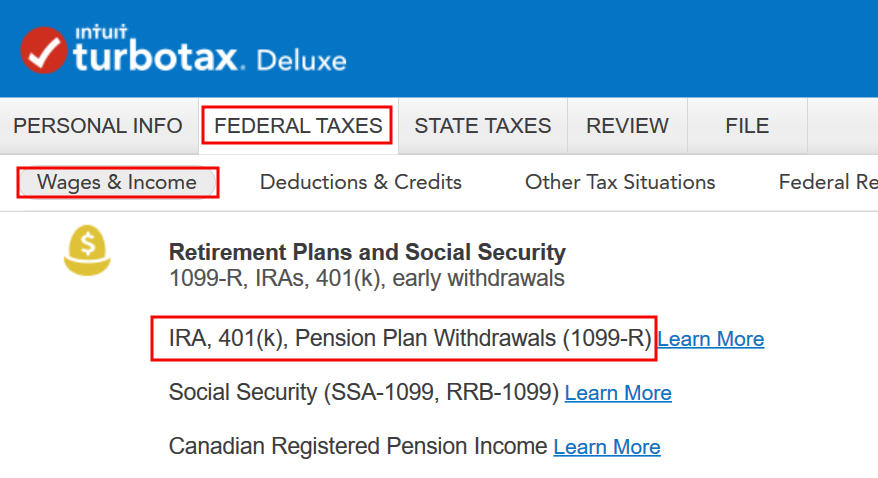

Enter 1099-R

Go to Federal Taxes -> Wages & Revenue -> IRA, 401(ok), Pension Plan Withdrawals (1099-R).

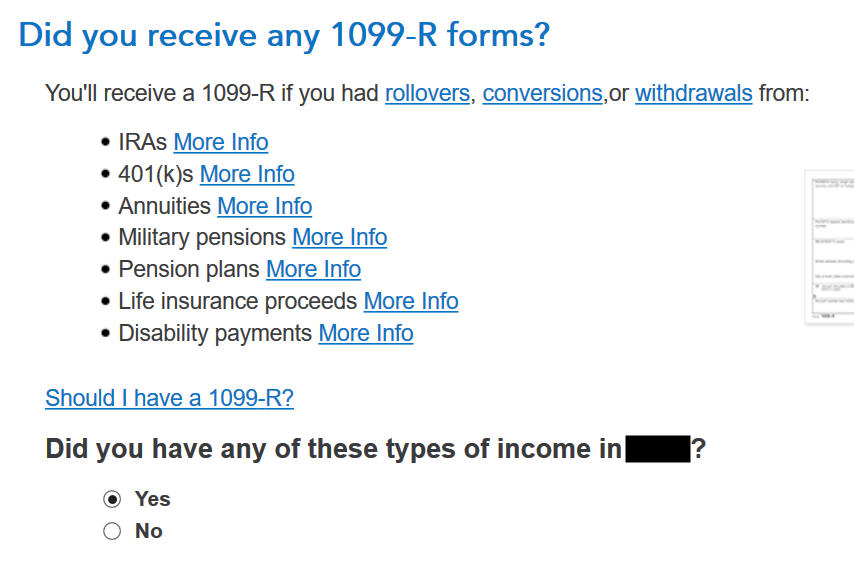

As you’re employed via the interview, you’ll ultimately come to the purpose of getting into the 1099-R. Choose Sure, you’ve gotten such a revenue. Import the 1099-R should you’d like. I’m selecting to sort it myself.

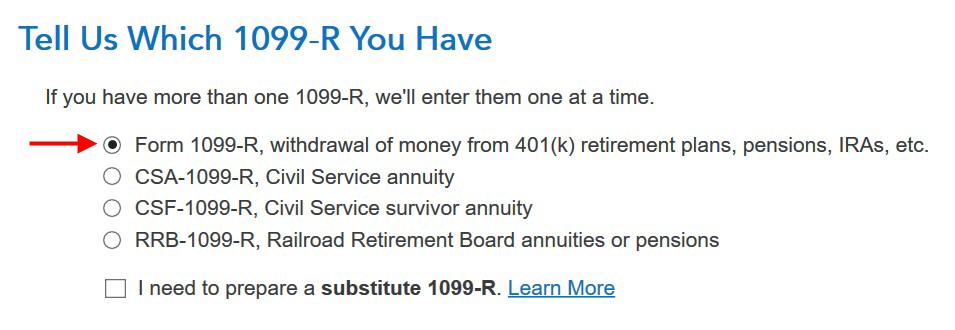

Simply the common 1099-R.

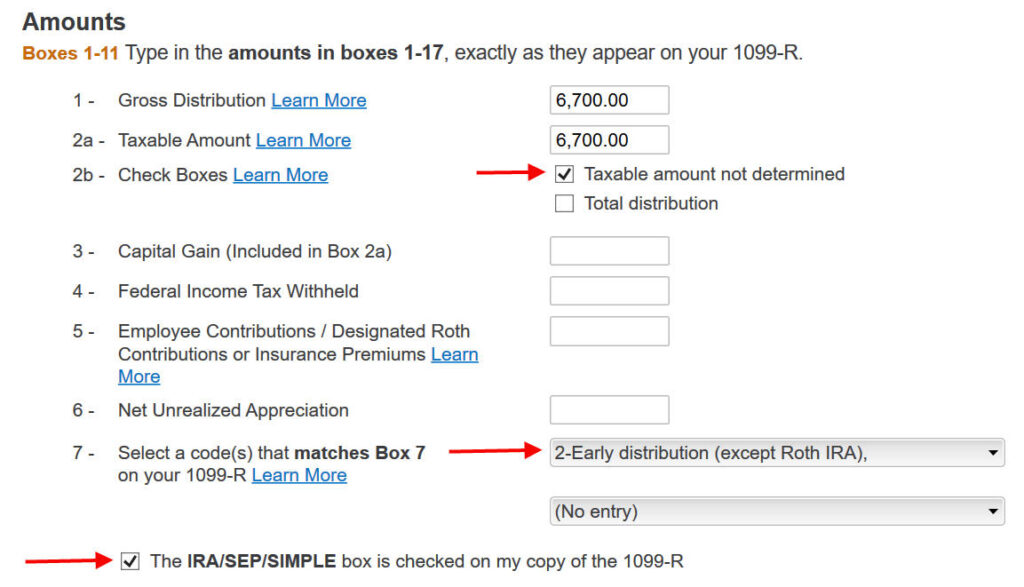

Field 1 reveals the quantity transformed to the Roth IRA. It’s regular to have the identical quantity because the taxable quantity in Field 2a when Field 2b is checked saying “taxable quantity not decided.” Take note of the code in Field 7 and the IRA/SEP/SIMPLE field. Be sure your entry matches your 1099-R precisely.

You get this Good Information, however …

Your refund in progress drops so much. We went from $2,384 all the way down to $858. Don’t panic. It’s regular and momentary.

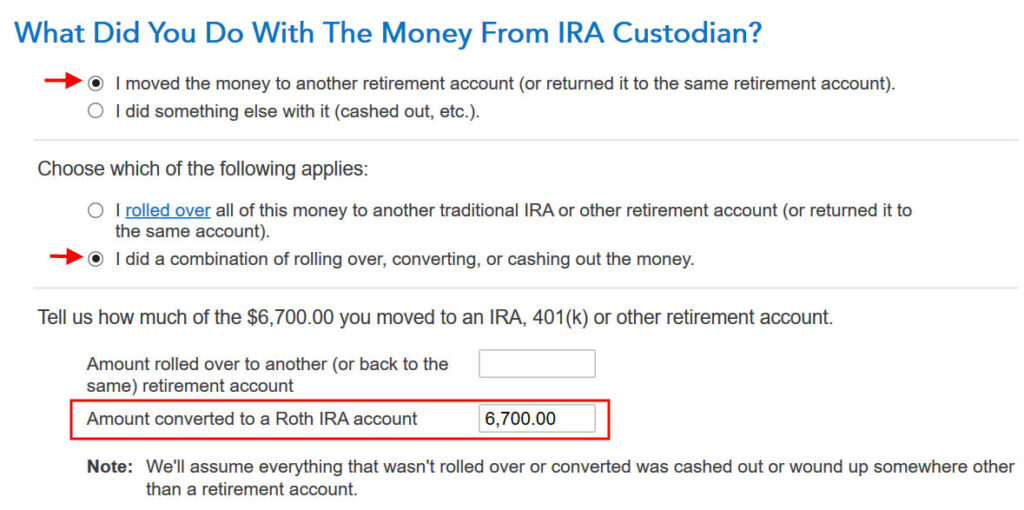

Transformed to Roth

Didn’t inherit it.

First click on on “I moved …” then click on on “I did a mix …” Enter the quantity transformed within the field. Don’t select the “I rolled over …” choice. A Roth conversion shouldn’t be a rollover.

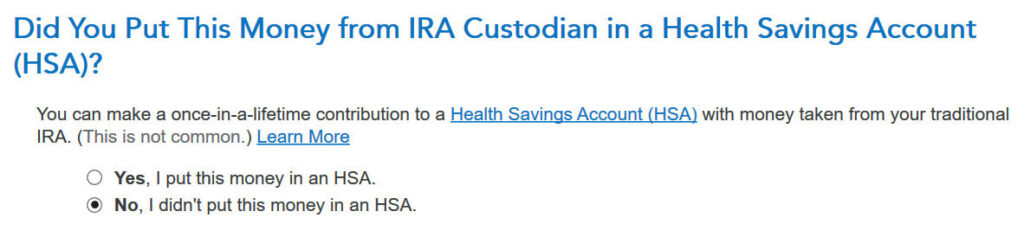

No, you didn’t put the cash in an HSA.

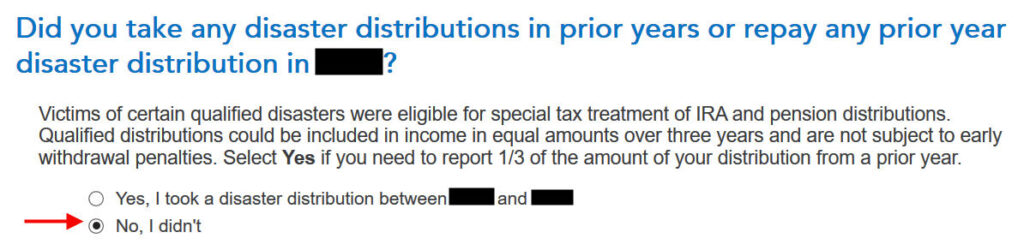

Not as a consequence of a catastrophe.

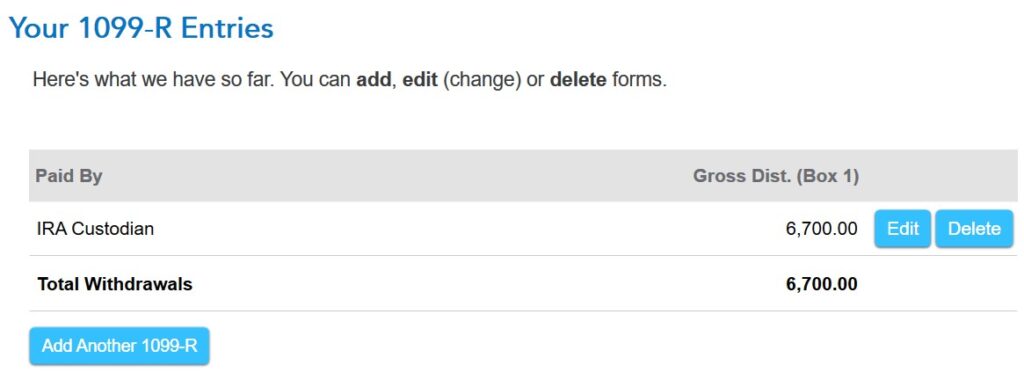

You get a abstract of your 1099-R’s. Repeat the earlier steps so as to add one other when you’ve got a couple of. Should you’re married and each of you probably did a Backdoor Roth, enter the 1099-R for each of you, however take note of choose whose 1099-R it’s. Don’t by chance assign two 1099-R’s to the identical particular person.

Foundation and Finish-of-Yr Values

Didn’t take or repay any catastrophe distribution.

Right here it’s asking concerning the prior 12 months carryover. Whenever you’re doing a clear “deliberate” Backdoor Roth as in our instance — contribute for 12 months X in 12 months X and convert earlier than the tip of 12 months X — you’ll be able to reply No right here. Should you contributed for the earlier 12 months between January 1 and April 15 throughout 12 months X, reply Sure right here.

Should you answered Sure to the earlier query and you probably did your earlier 12 months’s return accurately additionally in TurboTax, your foundation from the earlier 12 months will present up right here. Should you did your earlier 12 months’s tax return unsuitable, repair your earlier return first.

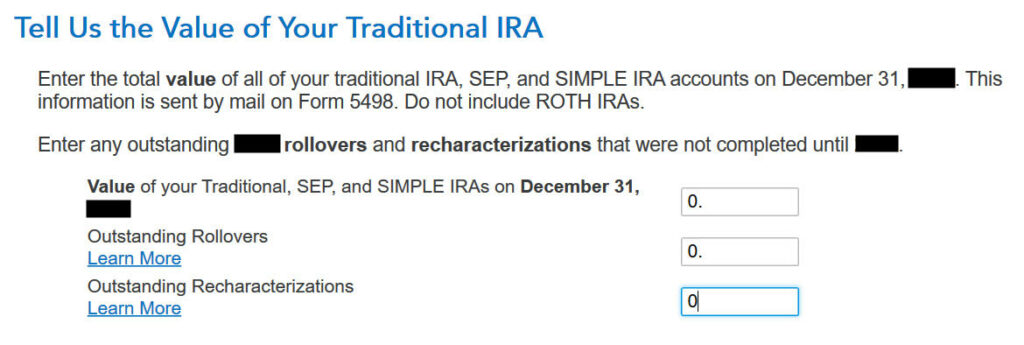

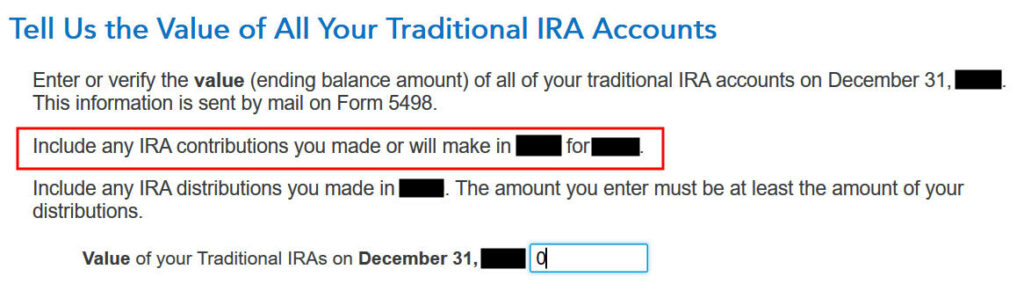

Enter the values on the finish of the 12 months. We don’t have something in conventional, SEP, or SIMPLE IRAs after we transformed all of it.

That’s it thus far on the revenue aspect. Proceed with different revenue gadgets. The refund in progress remains to be briefly depressed. Don’t fear. It’ll change.

Non-Deductible Contribution to Conventional IRA

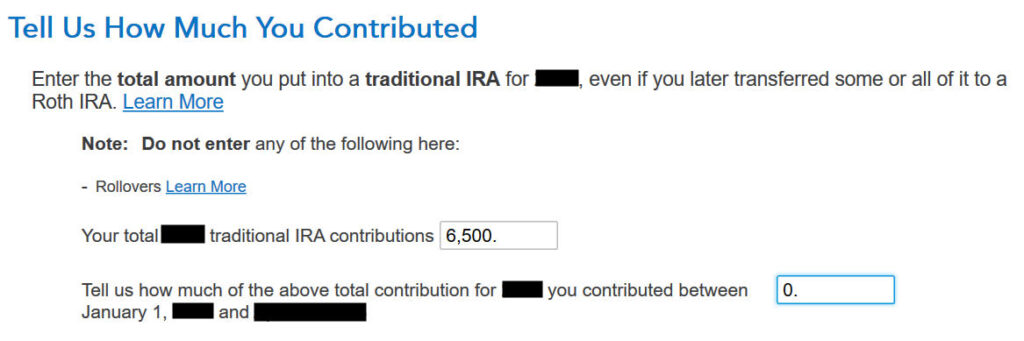

Now we enter the non-deductible contribution to a Conventional IRA *for* the 12 months we’re doing the tax return.

Full this half whether or not you contributed earlier than December 31 otherwise you did it or are planning on doing it within the following 12 months between January 1 and April 15. In case your contribution in the course of the 12 months in query was for the 12 months earlier than, be sure you entered it on the earlier tax return. If not, repair your earlier return first.

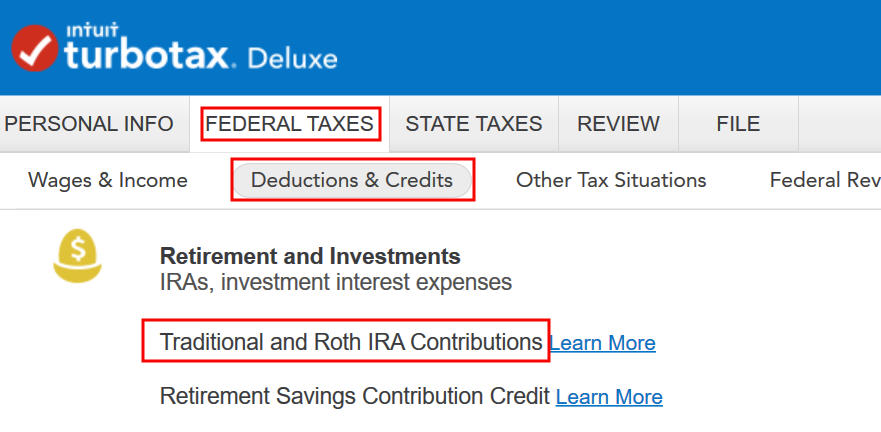

Go to Federal Taxes -> Deductions & Credit -> Conventional and Roth IRA Contributions.

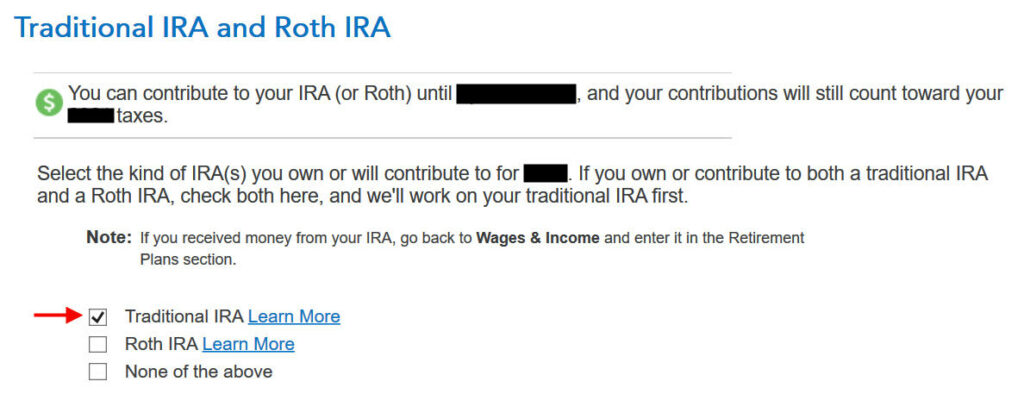

As a result of we did a clear “deliberate” Backdoor Roth, we examine the field for Conventional IRA. Should you did a detour while you first contributed to a Roth IRA earlier than you realized your revenue is simply too excessive and also you recharacterized the contribution as to a Conventional IRA, examine the field for Roth IRA and reply the questions accordingly.

TurboTax affords an improve however we select to proceed in TurboTax Deluxe.

We already checked the field for Conventional however TurboTax simply desires to verify. Reply Sure right here.

It was not a compensation of a retirement distribution.

Enter the contribution quantity. As a result of we contributed for 12 months X in 12 months X, we put zero within the second field. Should you contributed for the earlier 12 months between January 1 and April, enter the contribution in each bins.

Straight away our federal refund in progress goes again up! We began with $2,384. It went all the way down to $858. Now it comes again to $2,335. The $49 distinction is as a result of we’ve got to pay tax on the $200 in earnings once we contributed $6,500 and transformed $6,700. Should you had much less earnings, your refund numbers could be nearer nonetheless.

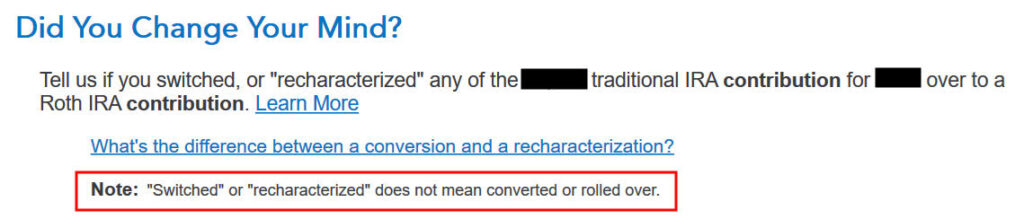

It is a essential query. Reply “No.” You transformed the cash, not switched or recharacterized.

You could not get this query should you already entered your W-2 and it has Field 13 for the retirement protection checked. Reply sure should you’re lined by a retirement plan however the field in your W-2 wasn’t checked.

No extra contribution.

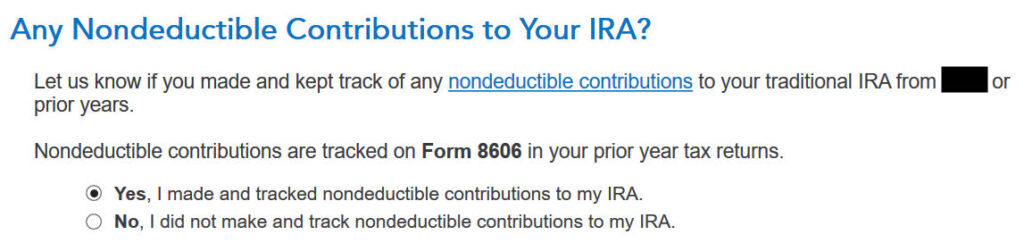

Identical query we noticed earlier than. For a clear “deliberate” Backdoor Roth, we are able to reply No. Should you made non-deductible contribution for earlier years, reply Sure.

Complete foundation via the earlier 12 months. Should you did your taxes accurately on TurboTax final 12 months, TurboTax transfers the quantity right here. Should you made non-deductible contributions for earlier years (no matter when), enter the quantity on line 14 of your Kind 8606 from final 12 months.

As a result of we did a clear “deliberate” Backdoor Roth, we don’t have something left after we transformed every thing earlier than the tip of the identical 12 months.

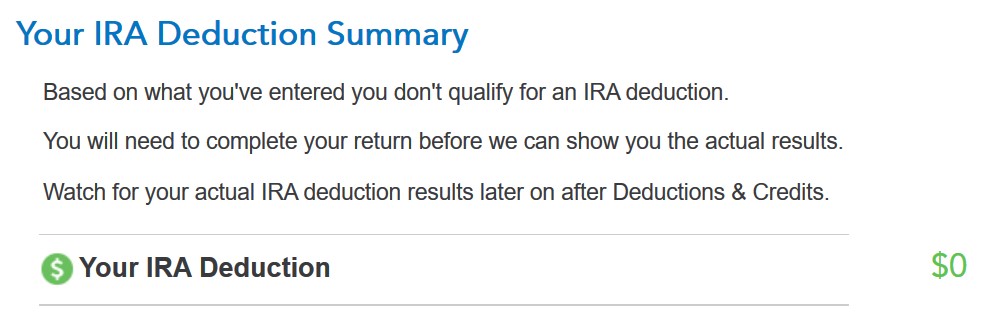

Revenue too excessive. We all know. That’s why we did the Backdoor Roth.

The IRA deduction abstract reveals $0 deduction, which is anticipated.

Taxable Revenue from Backdoor Roth

After going via all these, would you wish to see how you’re taxed on the Backdoor Roth?

Click on on Varieties on the highest proper.

Discover Kind 1040 within the left navigation panel. Scroll up or down on the best to search out strains 4a and 4b. They present a $6,200 distribution from the IRA and solely $200 of the $6,200 is taxable. That’s the incomes between the time you contributed to your Conventional IRA and the time you transformed it to Roth.

Whenever you’re finished analyzing the shape, click on on Step-by-Step on the highest proper to return to the interview.

Tah-Dah! You place cash right into a Roth IRA via the backdoor while you aren’t eligible to contribute to it instantly. That’s why it’s known as a Backdoor Roth. You pay tax on a small quantity in earnings should you waited between contributions and conversion. That’s negligible relative to the advantage of having tax-free development in your contributions for a few years.

Troubleshooting

Should you adopted the steps and you aren’t getting the anticipated outcomes, right here are some things to examine.

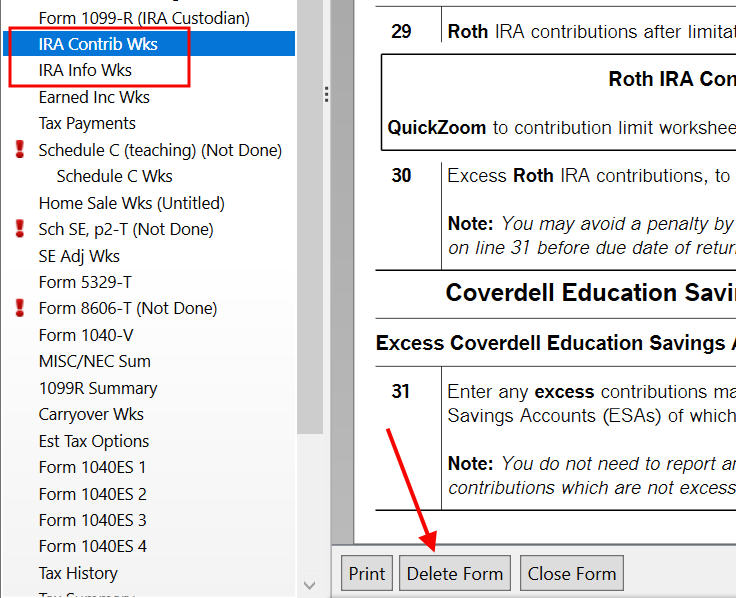

Contemporary Begin

It’s greatest to observe the steps contemporary in a single move. Should you already went forwards and backwards with totally different solutions earlier than you discovered this information, a few of your earlier solutions could also be caught someplace you now not see. You may delete them and begin over.

Click on on Varieties on the highest proper.

Discover “IRA Contrib Wks” and “IRA Information Wks” within the left navigation pane and click on on “Delete Kind” to delete them. Then you can begin over by following the steps above.

W-2 Field 13

Be sure the Retirement Plan field in Field 13 of the W-2 you entered into the software program matches your precise W-2. If you’re married and each of you’ve gotten a W-2, be certain that your entries for each W-2’s match the precise varieties you obtained.

If you end up not lined by a retirement plan at work, corresponding to a 401k or 403b plan, your Conventional IRA contribution could also be deductible, which additionally makes your Roth conversion taxable.

Self vs Partner

If you’re married, be sure you don’t have the 1099-R and IRA contribution combined up between your self and your partner. Should you inadvertently entered two 1099-Rs issued to you rather than one for you and one in your partner, the second 1099-R to you’ll not match up with a Conventional IRA contribution made by your partner. Should you entered a 1099-R for each your self and your partner however you solely entered one Conventional IRA contribution, you may be taxed on one 1099-R.

Say No To Administration Charges

If you’re paying an advisor a proportion of your property, you’re paying 5-10x an excessive amount of. Learn to discover an unbiased advisor, pay for recommendation, and solely the recommendation.

[ad_2]